While the researchers disclosed their funding source for the 2011 paper “Do Payday Loans Trap Consumers in a Cycle of Debt?” they also assured readers that the industry “exercised no control over the research or the editorial content of this paper.”

The assertion was patently false, according to correspondence obtained from Arkansas Tech University through an open records request by the watchdog group Campaign for Accountability. The group subsequently shared the documents with HuffPost.

The Campaign for Accountability has filed requests for documents from professors at three other universities -- the University of California, Davis; George Mason University; and Kennesaw State University -- who produced similar pro-industry studies. So far, it has been met with resistance. Only Arkansas Tech turned over a cache of its records.

The emails show that the payday loan industry gave economics professor Marc Fusaro at least $39,912 to write his paper, and paid an undisclosed sum to his research partner, Patricia Cirillo. In return, the industry received early drafts of the paper, provided line-by-line revisions, suggested deleting a section that reflected poorly on payday lenders, and even removed a disclosure detailing the role payday lending played in the preparation of the paper.

Hilary Miller, the president of the Payday Loan Bar Association, a lawyers' group for the industry, worked closely with the researchers on their study. Miller has represented payday lending giant Dollar Financial, and is also the president of the pro-industry group the Consumer Credit Research Foundation.

"This revelation has significant implications for the other research that the Consumer Credit Research Foundation has funded," an industry expert told HuffPost. The foundation’s website lists six studies that it has funded in whole or part, all of which have influenced political debate over payday lending. Papers funded by the CCRF, by academics affiliated with George Washington University and the University of North Carolina at Greensboro, among others, have argued that payday lenders do not target black neighborhoods, that there is no good reason to regulate payday loans to the military, and that payday loans are cheaper for consumers than fees tied to bounced checks.

The Consumer Financial Protection Bureau will release a draft of of the first-ever federal rules regulating payday loans before the end of the year

The connection between a pro-payday loan group and academic research comes as there is increased focus on the financial industry's influence over what are apparently neutral studies. Last month, economist Robert Litan ended his affiliation with think tank the Brookings Institution after Sen. Elizabeth Warren (D-Mass.) criticized him for failing to adequately disclose that mutual fund behemoth Capital Group had funded one of his papers. Think tank research in Washington has become increasingly suspect as special-interest money has found such validation useful in the lobbying process.

Academic research is broadly considered to have more integrity. But documents shared with HuffPost show that in May 2011, a full six months before the Arkansas Tech paper was published in November, Fusaro emailed Miller to say that he was “pushing forward” on the revisions Miller had sent him. Miller also provided Fusaro with detailed line edits in July, August and November.

Beyond detailed revisions, Fusaro also added to the paper at Miller’s suggestion at least twice. After doing this, he updated Miller to let him know that “we have edited sections 1 & 2 as you suggested.”

Fusaro also added wording drafted by Miller himself. The emails show that in September, Miller sent Fusaro three paragraphs to be included in the paper. A few days later, Fusaro emailed Miller saying “I already incorporated the wording you sent...”

Fusaro did not include at least two significant portions of the paper that Miller did not like. First, Miller expressed concern at a finding that many payday loan borrowers have significant and frequent debit overdrafts in the month before they borrow a payday loan. Lending to borrowers with recently negative bank balances would undercut the industry’s assertion that it provides credit to people who can afford it. Fusaro’s co-author, Cirillo, told him in an email that she thought Miller wasn’t “too happy” about the finding and that Miller said it wasn’t the “objective of the study.” Fusaro did not include a section on bank overdrafts in the paper.

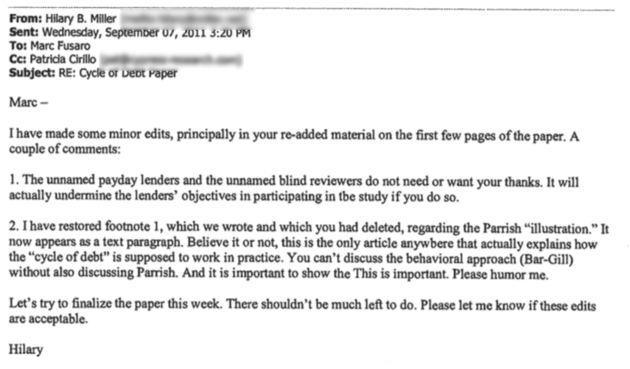

Miller also requested that Fusaro remove a portion of the author’s note that disclosed that payday lending companies had cooperated with the study. “The unnamed payday lenders and the unnamed blind reviewers do not need or want your thanks,” Miller said. “It will actually undermine the lenders’ objectives in participating in the study, if you do so.” Fusaro did not mention the involvement of the payday lenders in the author’s note.

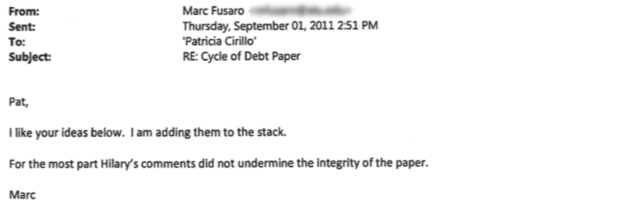

In one email to Cirillo, Fusaro defended -- though with qualifications -- Miller’s involvement in drafting, editing and removing material from the paper. “For the most part, Hilary's comments did not undermine the integrity of the paper,” Fusaro wrote.

For the study, the researchers gave some borrowers an interest-free loan and others a regular loan to see how interest rates impacted whether borrowers were likely to keep taking out new loans. Payday loans often trap borrowers in a cycle of debt, with a 2009 study from the Center for Responsible Lending finding that people taking out new loans to repay old loans make up 76 percent of the payday market.

After the paper was published, Fusaro complained to Cirillo that “the industry has forgotten about me.” That could be, the industry expert who spoke to HuffPost explained, because “the industry got cold feet when they looked at the results...” Despite Fusaro and Cirillo’s pro-payday loan and anti-consumer protection rhetoric, “they actually found that the median borrower has to use eight loans in a row, whether or not they get a free first loan,” the expert said.

In other words, the data shows payday loan payments, irrespective of the interest rate, are simply unaffordable.

But the authors “airbrushed” the true implications of the paper’s findings, the industry expert said. Instead of making the unaffordability of payday loans the thrust of the paper, the researchers framed the damning evidence that loans force people into an ever deeper cycle of debt as support for the idea that consumers simply choose to take out payday loans over and over again because they like to.

Fusaro and Cirillo did not respond to requests for comment on their work. In an email to HuffPost, Miller did not address his own edits, additions or deletions.

"At the time of copy-editing, at the investigators’ request, we also incorporated the comments of two academic peer reviewers, each of whom was an economist at another academic institution. All of these edits were then approved by the investigators. The results of the experiment are unchanged and reported in full in the paper," he said.

For payday lenders, academic research isn’t just an intellectual exercise. Payday lenders are trying to create research that they can point to in order to argue against regulation. “Regulators are taking a hard look at the payday loan market, and the industry would like to be able to point to studies that suggest there is not a problem here," Nick Bourke, a payday loan expert at Pew Charitable Trust, told Huffpost. "But in fact, on most of these issues, a fair reading of the data shows that there is a problem."

That fact is well known to Miller, who said as much in an offhand remark in an email to the professor. "In practice, consumers mostly either roll over or default; very few actually repay their loans in cash on the due date (which you know)," Miller wrote to Fusaro, whom he was paying to author a paper arguing in the opposite direction.

Miller and the payday loan industry have cited Fusaro and Cirillo’s paper in filings with federal regulators.

Original Article

Source: huffingtonpost.com/

Author: Ben Walsh, Ryan Grim

No comments:

Post a Comment